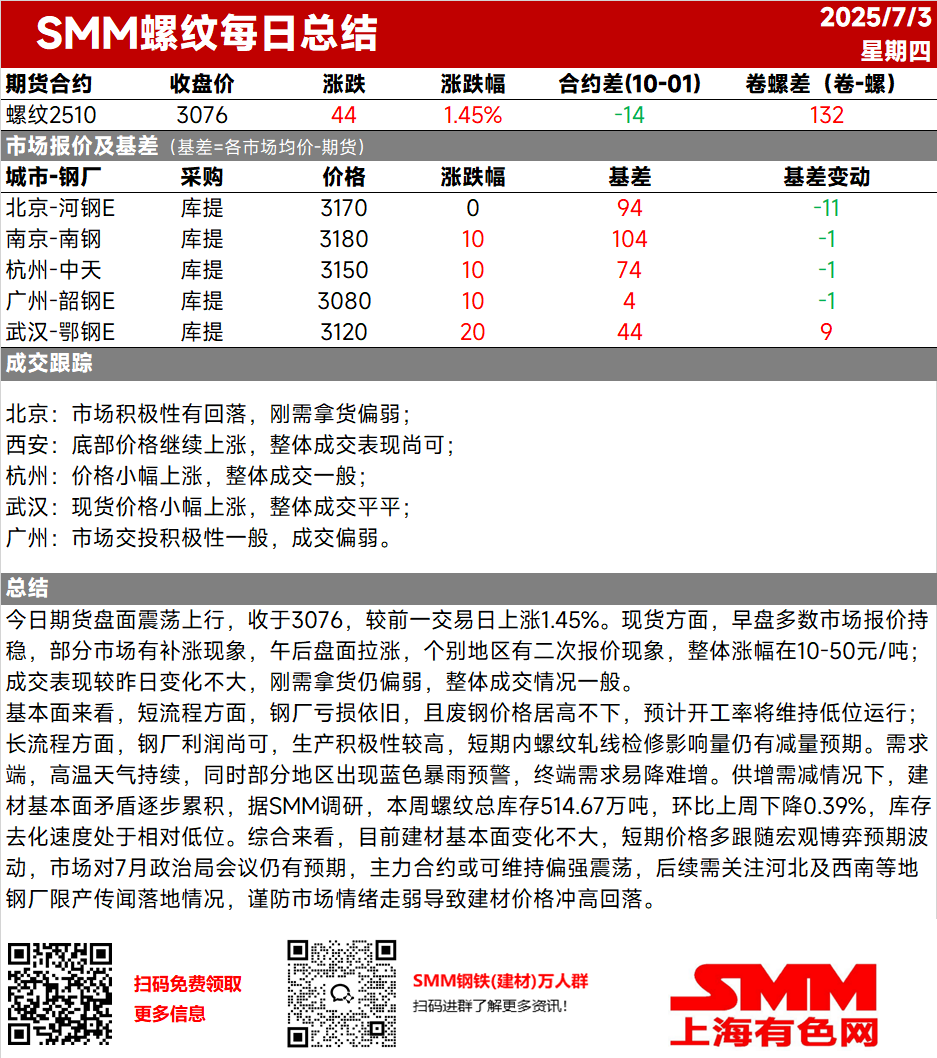

Today, the futures market fluctuated upward, closing at 3076, up 1.45% from the previous trading day. In the spot market, most market quotes held steady in the morning session, with some markets experiencing a catch-up rally. In the afternoon session, the futures market surged, leading to secondary quotes in individual regions. Overall, the price increase ranged from 10 to 50 yuan/mt. Trading activity remained relatively unchanged compared to yesterday, with weak rigid demand purchases and generally moderate trading conditions.

From a fundamental perspective, in the EAF sector, steel mills continue to face losses, and steel scrap prices remain high, which is expected to keep operating rates low. In the blast furnace sector, steel mill profits are moderate, and production enthusiasm is high. There is an expectation of a decrease in the impact from maintenance on rebar rolling lines in the short term. On the demand side, persistent high temperatures and blue rainstorm warnings in some regions make it difficult for end-use demand to increase and easy for it to decrease. With supply increasing and demand decreasing, the fundamental contradictions in the construction steel market are gradually accumulating. According to the SMM survey, the total rebar inventory this week was 5.1467 million mt, down 0.39% WoW, with inventory depletion at a relatively low rate. Overall, the fundamental situation in the construction steel market remains relatively unchanged. In the short term, prices are likely to fluctuate based on macroeconomic expectations. The market still has expectations for the July Political Bureau meeting, and the most-traded contract may hold up well. Subsequent attention should be paid to the implementation of production restriction rumors in steel mills in Hebei and southwestern regions, and caution should be exercised to prevent a market sentiment downturn leading to a jump initially and then pull back in construction steel prices.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)